What problems do fintechs need to solve to easily scale up and grow profits?

- Building an easily scalable software product

- Partnering with other companies and engaging new customer segments

- Complying with regulation and security standards while scaling up

In our guide we will dwell on how technologies can help you solve these 3 key challenges and build a fintech business that:

- generates profits,

- attracts investments,

- can achieve economies of scale.

About the guide

N-iX has cooperated with more than 15 successful fintechs including such market players as Currencycloud, RateSetter, and Cleverbridge, helping them use digital innovations to scale their businesses. Therefore, we have aggregated our experience in fintech app development and collected stats from such sources as CBInsights, Capgemini, PWC, Forbes, and more, to perform the comprehensive analysis of the critical scalability bottlenecks in fintech and establish the ways to eliminate them.

The report shows how technologies such as microservices, AI, blockchain, and others can help fintechs scale their software architectures and expand their market reach while complying with the security and regulatory standards. It also explains vital complexities associated with those technologies and critical strategies for their implementation.

As engineering resources are crucial for scaling a fintech business, we have dedicated special attention to the distribution of tech talent in Europe and North America, collecting data from LinkedIn and Glassdoor.com.

Part I. How to efficiently scale a software product

In their early days, fintech startups need to be lean and nimble. They are rushing to launch an MVP and market test their idea. However, the speed often comes with a tradeoff of software quality.

When fintech startups prove their idea viable and start scaling operations, it appears that their IT platform was not built with scalability in mind. That’s when they start facing critical software scalability challenges:

- Refactoring, as changes affect different platform components.

- Maintaining and scaling monolithic codebase.

- Changing the coding language.

- Managing and scaling a growing development team.

- Long time to market, as the codebase grows.

However, a reliable and easily scalable system goes a long way towards reducing operational costs and growing profits.

Thus, once the size of the codebase grows big, and changes need to be made promptly, many companies turn to microservice architecture.

Source: App. Dev. Survey

As microservices are loosely coupled, they can be scaled and deployed separately, which substantially reduces time to market and lowers costs. Microservices architecture helps to achieve:

- Scalability of a software development team.

- Independence of services and sub-teams.

- More efficient refactoring of services.

- Applying new technologies more easily.

- Adding new functionality more efficiently.

- Better internal and external API-driven integration.

1.1 Microservices adoption strategies

Depending on specific needs of fintechs, there are different microservices adoption strategies:

Building microservices architecture from the very beginning. This is a costly and time-consuming process, and early-stage startups rarely go for microservices from the start. As the codebase is small, a company can do just fine with a monolith architecture for the years.

Refactoring the monolith into microservices. If a codebase grows too big to be quickly scaled and maintained, a fintech decides to migrate to microservices. However, that means you need to maintain the old system, gradually refactor to microservices, and handle orchestration of microservices while in production.

The process is always technically complex, costly, and may take up to a year of development time. Companies often resort to this approach when they face the problem of engineering team scalability.

Adding new microservices to a monolith. Sometimes a company decides to keep the monolith and build new microservices around it. This strategy has its cost-and-time-saving benefits, but it’s not a future-proof approach as it will be much more complicated to completely refactor the monolith when the solution grows bigger.

That was the case of RateSetter, a P2P fintech that undergoes a partial transition to microservices architecture with the help of N-iX.

Splitting big microservices into smaller ones.

When microservices architecture is not correctly structured from the very beginning, it works inefficiently and calls for changes.

A payment fintech Currencycloud partnered with N-iX to restructure an already existing microservices architecture. As the services became too bulky, they wanted to break them into smaller, more efficient components.

1.2 Challenges of adopting microservices

Whatever strategy a fintech decides to take, microservices architecture adoption is a highly demanding task.

Let’s take a closer look at the challenges that are related to refactoring of an existing monolithic application.

Technological challenges of microservices adoption:

- Defining the microservices and their responsibility areas. Ideally, each service has to cover only one functionality, but they should not be too fine-grained as well. Otherwise, it will create too much communication between services and, consequently, increase performance overhead.

- Integration between microservices written with different technologies.

- Automatic deployment, scaling and managing the services.

- Fault-tolerant design of microservices to handle instances when a service is under heavy load and doesn’t respond.

- Handling the orchestration of microservices while in production.

- Managing multiple different databases.

- Easily searchable logging and monitoring of the whole system, with automatic notifications of a service failure.

- Automation test coverage to prevent defects while refactoring.

The organizational challenge of microservices adoption

Transitioning to microservices architecture calls for changing the structure of development teams. Teams need to be independent, have their areas of responsibility, and deploy separately, at their own time.

Source: Challenges when moving from monolith to microservices architecture

The cost-related challenge of microservices adoption

Migration to microservices architecture is time-consuming, requires complex expertise, and is costly. The critical cost-cutting strategy here is to decouple microservices and finetune the processes before the project’s start, as rework means multiplying person-hours and expenditures.

Another important aspect is finding experts with the best cost-quality ratio.

Talent-wise challenge of microservices adoption

Microservices is a complex, distributed system that requires experienced software engineers, DevOps specialists, automation testers, and, most important, experienced software architects with the corresponding domain expertise.

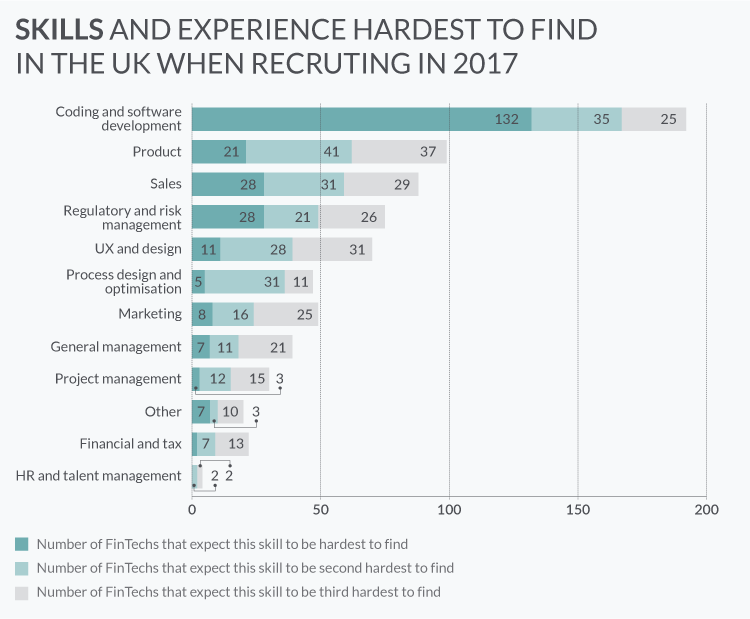

In fact, 58% of respondents cited attracting qualified or suitable talent as the most significant challenge for fintechs.

Due to the rapid information technology advancements, and soaring demand for qualified experts, the European Commission expects the shortage of IT-skilled staff could amount to 825,000 by 2020.

Source: FinTech Census 2017

What’s more, it is challenging to find managers with the tech expertise able to lead the whole development process.

As a result, there is fierce competition for experienced software developers, architects, and product managers in the UK, Europe, and the US, which drives their salaries up.

As the critical adoption challenges are technological complexity, lack of talent, and a high cost of implementation, many companies find it sensible to outsource their microservices architecture development to third-party vendors in Eastern Europe and Asia.

Eastern Europe alone offers a large talent pool, wide-ranging expertise, and optimum cost-quality ratio.

Part II. How to find new revenue streams

When fintechs find the technological capacity to build a scalable and reliable solution and manage to keep their operational costs low, they want to grow bigger, raise profits, and scale their business reach. However, that may be a daunting task due to strong cards of other financial services companies operating in the market.

Fintechs started as companies that began ‘unpackaging’ a traditional bundle of financial services. They aimed at creating a focused and highly effective user experience while filling a single niche. However, this competitive advantage greatly limits their potential market reach now.

Fintechs currently face severe competition with Big Techs such as Amazon, Google, Facebook, Apple, Tencent, which choose different points of entry into the financial domain and capitalize extensively on Big Data customer analytics and customer-facing AI.

What’s more, banks are still the one-stop-shop that is associated with a full package of financial operations. Banks have a few aces up their sleeve including a large customer base, a low cost of capital, and established brands.

As we can see, fintechs laid a strong foundation for innovation, but many of them now face the challenge of extending their market share, enhancing visibility, and achieving economies of scale.

To solve the problem, fintechs often decide to build bridges with traditional financial organizations. And the partnership can be mutually beneficial for both.

As Accenture estimates, full-service banks could lose 35% of their market share to more digitally mature competition by 2020. Furthermore, banks are now burdened with new regulations and open API demands. And they call for digital help.

As a result, one of the strongest fintech trends in 2018 is re-bundling of financial services and collaboration between fintechs and traditional financial companies.

Source: World FinTech report 2018

2.1 Collaboration between fintechs and finance companies. Key engagement models

Partnerships can be performed on different levels of integration. This can be an exchange of limited sets of data, e.g. a P2P fintech informs a bank about potential lenders, and a bank buys those loans from a fintech.

Banks and fintechs can also engage in a much deeper collaboration, creating shared digital platforms that utilize incumbent’s large investment share.

As integration is often complex and challenging, some fintechs and financial companies decide to choose an arm-length cooperation model.

For instance, in its partnership with BBVA Bancomer, Destacame has a completely separate system from the bank.

Source: How Financial Institutions and Fintechs Are Partnering for Inclusion: Lessons from the Frontlines

However, there are multiple engagement models preferred by Fintechs

Source: World FinTech report 2018

White-label solution. An incumbent purchases a product from a fintech and markets it under its own name. Thus fintechs can have a one-to-many service model, offering their solution to multiple incumbents without being fully committed to just one. The traditional firm’s brand name, infrastructure, and a distribution network enable them to promptly bring the solution to the market.

Integrated in-house solutions. A traditional firm hosts a fintech solution in-house or as software-as-a-service (for small firms). However, that calls for complex integration and may pose a challenge.

Full outsourcing. This model means financial institutions outsource their non-core capabilities to a fintech firm.

API integrations. A traditional firm provides APIs, so fintechs get access to their data and can deliver different operations. In another scenario, an incumbent leverages APIs that have been offered by a fintech firm. We will dwell on APIs in more detail in chapter 2.3.

Standalone in-house solutions. In this engagement model, a traditional financial services company uses the fintech’s technology as a stand-alone in-house platform. However, integrating a technology with an incumbent’s legacy system may be a daunting task.

Accelerator and Incubator programs. Incumbents create accelerators and incubators for fintechs to develop innovative solutions.

2.2 Fintechs and financial companies cooperate to extend their market reach

As both fintechs and financial services companies strive for extending their market shares, they cooperate to enable financial inclusion of the unserved and under-served customers.

Fintechs offer agility, emerging technologies, and cost-effective solutions. Incumbents provide a trusted brand, infrastructure, and access to capital. According to the report, they form a symbiotic relationship that helps to achieve the following goals:

- Access new market segments

Financial institutions and fintech companies partner to engage the unbanked and underbanked population in remote areas where brick-and-mortar branches are unprofitable.

Cases:

AXA is collaborating with MicroEnsure to expand its customer reach. AXA used to cover only the most wealthy 5-10% of customers in emerging markets. MicroEnsure, a specialist provider of insurance offered AXA an IT platform designed to serve large numbers of customers at lower costs.

AXA says that its partnership with MicroEnsure has allowed the company to form better partnerships with mobile network operators (MNOs) because MicroEnsure also brings integration experience with telco systems.

The collaboration has reduced operational costs and enabled AXA to extend coverage to 10 million low-income customers across Africa and Asia. Meanwhile, MicroEnsure continues to build solid partnerships with many MNOs and other insurance companies.

Diamond Trust Bank (DTB) is partnering with Kopo Kopo in Kenya and Uganda to provide services to retail merchants.

Mastercard is partnering with Grindrod Bank and Net1 to reach unbanked population segments in South Africa.

- Create new offerings for existing customers

Another goal is to create profitable services for existing customers in the lower market segments.

Case:

ICICI Bank, a large bank in India, is partnering with Stellar, a Silicon Valley-based non-profit company which offers distributed ledger payments network to its customers. Following the establishment of 300,000 accounts, the bank will pay Stellar a fee for each additional account.

- Collect, store, and analyze data

Additional important focus is leveraging Data Science and AI to improve user experience and access more customers.

Cases:

The BBVA Bancomer is partnering with Destacame, an alternative credit scoring platform, to increase credit access to customers with thin credit history in Latin America through data analytics.

In Spain, MicroBank is partnering with EFL, a psychometric scoring platform, to extend credit access to underserved SMEs.

DemystData, a New York-based software as a service provider, started as an alternative credit scoring platform and has extended its operation to data testing, cleaning and standardization for enhanced data access and compliance. One of its clients is a major bank in the Philippines.

- Deepen customer engagement and product usage

To access underserved low-income customers, inform them about new services and potentially expand their usage of financial products, companies need constant interaction and digital immersion into their users’ everyday life.

Cases:

For instance, MetLife is partnering with Imaginate, a virtual reality and augmented reality software development company. They aimed to design an immersive customer journey for insurance policyholders in India. In this virtual branch, users can interact with insurance agents, get information, and submit claims.

In Latin America, BBVA Bancomer and Bancolombia are each working with Juntos, an AI fintech company. The two banks use Juntos’ platform to communicate with their customers via automated and customized messages.

Partnerships between fintechs and incumbents could follow very different roads. In some cases, incumbents and fintechs can continue to cooperate as partners. In other cases, a financial institution might buy the technology from a fintech or learn more about the technology and start its own development.

2.3 API – a secure connection for cooperation

To enable the integration of two separate systems, API technology comes in handy. API, which has been around for many years for coordination of internal components, is now widely used for effective business-to-business integrations (mainly Soap and Rest services).

An API is a secure gateway between software systems that allows accessing data in a controlled way. For instance, a third party can access financial institution’s customer data through an API.

Benefits of APIs:

- Have the capacity to automate processes

- Provide secure access to data to a third party

- Allow integrating with third-party products

- Allow for customer identity authentication

- Enable different levels of integration

According to Fintech Ranking, multiple types of fintech APIs fall into several categories:

- Core banking (for deposits, lending and SME cross-border)

- Plug & Play (trading, accounting routine, oAuth)

- Cards, wallets, and transfers (SDK stock, MultiCurrency, fraud monitoring and others)

- Acquiring (mobile and alternative phone payments, NFC solution, online card purchasing, and others)

The PSD2 directive, which started applying from 13 January 2018, gave a huge boost to API development. As more financial companies are now taking the effort to comply with open API demands of the PSD2, the need for skills has seen a considerable year-on-year increase: API Development (70%), API Integration (107%) and API Testing (83%).

What’s more, the complexity of banks’ legacy systems makes API development and integration extremely challenging.

Hans Tesselaar, executive director at Banking Industry Architecture Network (BIAN), a non-for-profit fintech industry body, says:

The real challenge for banks is that they have to connect to their complex back office environment before they are able to work on implementing open APIs. This is something that fintechs do not have to do, resulting in a much faster and more efficient integration process than banks.

Additionally, usage of open APIs in financial operations calls for their standardization. To address the need, the National Automated Clearing House Association (NACHA) set up the API Standardization Industry Group in May. Its aim is to design an “API Playbook” that will aid banks, fintechs, and other financial institutions in consolidating their view of APIs.

So far, its members include such leading market players as JP Morgan, Wells Fargo, Intuit and the Bank of America, as well as big credit card companies, Visa and MasterCard, and the group is still open to new members.

According to PWC Global Fintech report, regulatory uncertainty and IT security are among the key stumbling blocks in the cooperation between fintechs and incumbents.

Source: PWC Global Fintech report

Part III. How to scale up without compromising security

As companies scale transaction volumes and integrate with more and more third parties, they get a growing inflow of data and business insights. On the downside, this subsequently increases the risk of data breaches and cyber attacks.

According to Forbes, the overall global cost of cybercrime is predicted to total $2.1 trillion by 2019 which is 400% more than in 2015.

Primarily, that is a hot topic for financial services companies and fintechs in particular. According to the research findings, fintech companies are prime targets for cybercrime attacks with the growth of attacks outpacing transactional increase by 50%. – Thinkadvisor

ThreatMetrix research showed 80% increase in digital wallet transactions year-on-year as well as a 180% increase in associated bot attacks, that are used to mass test identity credentials.

Also, fintechs currently suffer from the mismatch between innovations and regulations as the latter don’t keep up with the technological advancement in the financial industry.What’s more, early-stage startups usually don’t have adequate compliance teams. Such unstable regulatory environment creates additional security and compliance challenges for the financial market players.

There are two key technologies which will play a key role in cybersecurity.

3.1 AI and Machine Learning

According to the report, the AI in fintech market is expected to grow from USD 1,337.7 million in 2017 to USD 7,305.6 million by 2022, at a CAGR of 40.4%,

There are four major areas in fintech software development where AI is making a game-changing effect:

- Detection and prevention of cyber-security attacks.

- Predictions and recommendations on the customers’ credit-worthiness.

- Using capsule neural networks to identify customers and documents visually.

- Leveraging intelligent chat-bots.

To detect fraudulent financial behavior and prevent cyber-attacks, fintechs frequently use a generative adversarial network (GAN). GAN is a type of deep learning system that works as two competing neural networks: a generator and a discriminator.

The generator network creates fake data that looks identical to the real data. Whereas, the discriminator network analyses both synthetic data and the authentic dataset. Over time, both networks improve their results and learn from each other.

There are many fintechs that work in fraud detection and regulatory area.

Source: AI Fintech Startup Market Cap

However, we can see that financial incumbents are taking many AI-related initiatives, and they don’t want to lag behind.

According to PWC report, more than 30% of financial institutions are investing into AI.

Source: PWC report

According to a recent TCS study into AI across 13 sectors, 86% of business leaders in the banking and financial services sector said they were already using this technology.

According to reports, banks are mainly focusing on using AI for security and biometrics.

Source: Competitive Survival in Banking Hinges on Artificial Intelligence

Shortage of AI talent

Consequently, we can see a growing trend for the share of jobs that require AI skills.

Source: 10 Charts That Will Change Your Perspective On Artificial Intelligence’s Growth

Companies like Amazon, Google, and Facebook are alluring top AI talent with high salaries and high perks. Big banks also have more capital than fintechs to compete for it. As a result, the latter face a severe problem of AI talent shortage.

According to the analysis of glassdoor.com search results, we can see that the demand for AI and Machine learning specialists is great. Companies in the UK are looking for 4,525 AI specialists and 4,859 Machine learning engineers. In the US, the demand is even bigger – companies are looking to engage 33,607 AI specialists and 53,579 Machine learning experts.

To face the challenge, many fintechs are looking for AI talent in Eastern Europe, and for a good reason. According to the LinkedIn search results, Eastern Europe has a talent pool of 15,254 AI specialists and 21,035 Machine learning engineers.

3.2 Blockchain and Distributed Ledger Technology

The blockchain is another hot topic in fintech. The technology is predicted to reinforce the security of financial operations.

In Forbes’ third edition of the “Fintech 50”, eleven companies use blockchain technology or are connected to the cryptocurrency industry.

According to KPMG’s Pulse of Fintech, blockchain companies raised record high $512 million of venture capital investment in Q4’17.

According to Statista, the size of global blockchain technology market is predicted to grow to 2.3 billion U.S. dollars by 2021.

Source: Statista

The distributed ledger technology doesn’t apply to all business cases. However, if its usage is well-grounded, it offers multiple benefits, including security, transparency, improved digital identity, and traceability of transactions.

Its principal use cases in fintech are smart contracts, smart assets (especially in trade finance), clearing and settlement, payments, digital identity (KYC), and cryptocurrencies.

A PWC research of the financial services sector and fintech has shown that around 77% of financial services industry leaders are looking to adopt blockchain in some way by 2020.

Banks have shown interest in the technology, with nearly one-third of surveyed institutions noting that they have started developing strategies to integrate blockchain into their financial operations. Banks partner with blockchain startups, invest in the blockchain research, and set up accelerators.

Source: Outlier Ventures

Goldman Sachs is setting up a cryptocurrency trading desk in New York that will be up and running by the end of June 2018.

Across the ocean, a Swiss bank UBS is leading a pilot that aims to automate regulatory requirements for the MiFID II/MiFIR rules that take effect in 2018.

Tech giants are not lagging behind as well. According to CBInsights, Google was the second most active corporate investor in blockchain tech from 2012 to 2017. And now Google is planning to adopt a blockchain-like ledger system, to differentiate its cloud business from the competition.

As we can see, both financial services incumbents and Big Techs are showing considerable interest in blockchain and, subsequently, luring blockchain talent.

The fight for blockchain talent

There is an astounding shortage of blockchain talent across the world, and the competition for is incredibly fierce.

The scarcity of blockchain specialists has its impact on the global market and companies that want to implement blockchain solutions. According to the findings of the poll conducted by Synechron and TABB Group, about 40% of firms do not have enough qualified blockchain engineers.

The shortage of available talent for blockchain was mentioned as a critical topic at the DTCC’s Fintech Symposium, held at the Grand Hyatt in New York City.

According to LinkedIn data, there are just around 75,000 blockchain and distributed ledger specialists in the US and about 16,000 in the UK. Eastern Europe offers an additional pool of roughly 7,500 blockchain engineers. That is a lucrative source of talent for Western companies that have a hard time finding relevant skills in their local markets.

Afterword

To beat the competition, fintechs need to prepare a solid ground for growth. They must have a reliable and easily scalable IT platforms to efficiently expand operations, innovate, develop new business models, cooperate with other companies, and reach new customer segments.

Fintechs use microservices architecture to overcome the challenges of software infrastructure scalability. API development enables effective business-to-business integration. Yet, scaling operations and integrating with third-party companies raise security issues. AI and Blockchain are the tech solutions that address those concerns.

However, demand for project talent causes fierce competition for it. Outsourcing to Eastern Europe and Asia may be one of the viable solutions that helps to overcome the engineering gap.

Sources

- KPMG, The Pulse of Fintech Q4 2017

- CBInsights, Fintech Trends 2018

- Forbes, Cyber Crime Costs Projected To Reach $2 Trillion by 2019

- Forbes, 10 Charts That Will Change Your Perspective On Artificial Intelligence’s Growth

- Nginx, App. Dev. Survey

- Researchgate, Challenges when moving from monolith to microservices architecture

- EY, FinTech Census 2017

- Empirica, Trends and Forecasts for the European ICT Professional and Digital Leadership Labour Markets (2015-2020)

- EY, UK FinTech: On the cutting edge: An evaluation of the international FinTech sector

- World Economic Forum, A pragmatic assessment of disruptive potential in financial services

- Center for Financial Inclusion, How Financial Institutions and Fintechs Are Partnering for Inclusion: Lessons from the Frontlines

- Capgemini, World FinTech report 2018

- Fintech Ranking, Bank as a Service

- Diginomica, PSD2 and the API challenge for Open Banking

- Thinkadvisor, Fintech Firms Primary Targets for Cybercrime Attacks

- ThreatMetrix, Cybercrime Report

- Markets and Markets, AI in Fintech Market

- Finextra, 4 AI Use Cases in Fintech in 2018 according to PwC and Gartner

- Techemergence, AI in Banking – An Analysis of America’s 7 Top Bank

- The Financial Brand, Competitive Survival in Banking Hinges on Artificial Intelligence

- Businesswire, Research and Markets report

- Finyear, The five major use cases for financial blockchains

- CBInsights, Blockchain Investment Trends in Review

- The Verge, Google is Adopting Blockchain-Like Technnology

- The Trade News, Lack of blockchain talent hindering implementation for 40% of firms

- ImpactLab, The lack of blockchain talent is becoming an industry concern

- Bloomberg, Goldman is setting up a cryptocurrency trading desk

- PWC, Global Fintech report

- Kalske M., Mäkitalo N., Mikkonen T. (2018) Challenges When Moving from Monolith to Microservice Architecture. In: Garrigós I., Wimmer M. (eds) Current Trends in Web Engineering. ICWE 2017. Lecture Notes in Computer Science, vol 10544. Springer, Cham